{kind=link}

If you’re thinking “i’m 25 and earning ₹30k a month how should i start investing for long-term growth?”, you’re already ahead of most people your age. Not because of how much you earn—but because you’re thinking in terms of systems, compounding, and long-term strategy.

This guide is not about quick wins or trendy investments. It’s about building a repeatable financial engine that works even with limited income—and scales as your income grows.

Table of Contents

The Reality Check: ₹30K Is Enough

At ₹30,000/month, you’re operating under resource constraints. That changes your investment strategy fundamentally:

- You can’t afford large mistakes

- You can’t rely on lump sum investing

- You must optimize for consistency over intensity

If you’re asking, “i’m 25 and earning ₹30k a month how should i start investing for long-term growth?”, the answer is not “invest more,” but “invest systematically.”

Step 1: Design Your Monthly Money Flow

Before investing, you need a cash flow architecture. Without this, even good investment choices fail due to inconsistency.

Ideal Allocation Model – ₹30K Income

| Category | % Range | Monthly Amount | Strategic Purpose | Notes |

|---|---|---|---|---|

| Essentials | 50–60% | ₹15K–₹18K | Survival stability | Try to cap this over time |

| Investments | 20–25% | ₹6K–₹7.5K | Wealth creation | Non-negotiable |

| Emergency Fund | 10–15% | ₹3K–₹4.5K | Risk protection | Temporary bucket |

| Lifestyle | 5–10% | ₹1.5K–₹3K | Sustainability | Prevent burnout |

What If You Can’t Hit 20%?

| Situation | Action |

|---|---|

| High rent | Reduce lifestyle, not investments |

| Family responsibilities | Start with 10% investing |

| Debt present | Prioritize high interest debt first |

Step 2: Build an Emergency Fund

If you skip this step, your entire investment plan is fragile.

When people ask “i’m 25 and earning ₹30k a month how should i start investing for long-term growth?”, they often ignore this—yet it’s the foundation of long-term investing.

Emergency Fund Targets

| Expense Level | Monthly Expenses | Target (3–6 Months) | Ideal Corpus |

|---|---|---|---|

| Low | ₹15K | ₹45K–₹90K | ₹90K |

| Moderate | ₹20K | ₹60K–₹1.2L | ₹1L |

| High | ₹25K | ₹75K–₹1.5L | ₹1.2L |

Where to Keep It

| Option | Liquidity | Risk | Returns | Best Use |

|---|---|---|---|---|

| Savings Account | High | Very Low | 2–4% | Immediate access |

| Liquid Mutual Funds | High | Low | 4–6% | Better than savings |

| Fixed Deposit | Medium | Low | 5–7% | Partial allocation |

Step 3: Start Investing — Keep It Simple

Complex portfolios are not better portfolios—especially at lower income levels.

Recommended Starter Portfolio

| Asset Class | Allocation | Instrument Type | Why It Works |

|---|---|---|---|

| Equity | 70% | Index Funds | Growth + simplicity |

| Debt | 20% | PPF / Debt Funds | Stability |

| Gold | 10% | ETFs / SGBs | Hedge against uncertainty |

Why This Works

- Equity drives long-term returns

- Debt reduces volatility

- Gold provides macro protection

Step 4: SIP — Your Core Growth Engine

If you’re wondering again, “i’m 25 and earning ₹30k a month how should i start investing for long-term growth?”, the most practical answer is: Start a SIP immediately.

You don’t need timing. You need discipline.

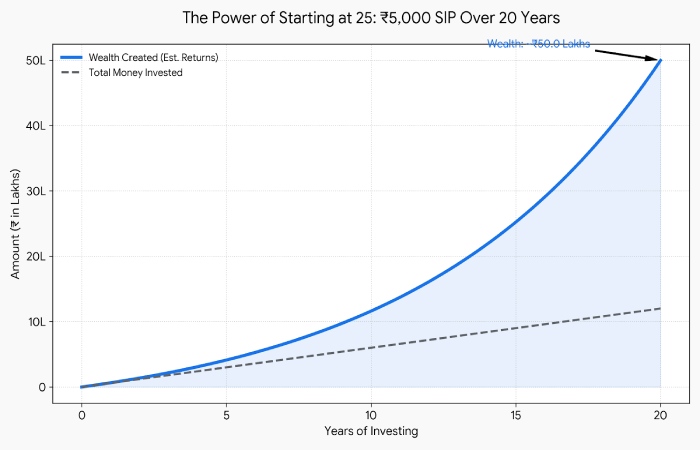

SIP Growth Projection (₹5,000/month)

| Time Horizon | Total Invested | Estimated Value (12%) | Wealth Multiplier |

|---|---|---|---|

| 5 Years | 3,00,000 | ₹4,12,000 | 1.37x |

| 10 Years | 6,00,000 | ₹11,50,000 | 1.9x |

| 15 Years | 9,00,000 | ₹25,00,000 | 2.7x |

| 20 Years | 12,00,000 | ₹49,00,000 | 4.1x |

Projected growth of ₹5,000 monthly SIP at 12% over 20 years—demonstrating the power of compounding.

Key Insight

| Phase | Growth Behavior |

|---|---|

| Years 1–5 | Slow |

| Years 5–10 | Moderate |

| Years 10–20 | Exponential |

Step 5: Best Investment Options in India

| Instrument | Risk | Return Potential | Lock-in | Ideal Role |

|---|---|---|---|---|

| Index Funds | Moderate | 10–12% | None | Core growth |

| PPF | Low | 7–8% | 15 years | Stability |

| ELSS | Moderate | 10–12% | 3 years | Tax saving |

| Gold ETFs | Low–Moderate | 6–8% | None | Hedge |

Step 6: Income Growth vs Investment Returns

This is where most beginners go wrong.

If you’re still asking “i’m 25 and earning ₹30k a month how should i start investing for long-term growth?”, understand this: Increasing income beats increasing returns.

Comparison

| Strategy | Monthly SIP | Return | 10-Year Value |

|---|---|---|---|

| Higher returns | ₹5K | 15% | ₹13.9L |

| Higher SIP | ₹10K | 12% | ₹23L |

Conclusion

| Lever | Impact |

|---|---|

| Better stock picking | Low |

| Increasing SIP | High |

| Career growth | Very High |

Step 7: Automation Strategy (Set and Forget)

Manual investing leads to inconsistency.

Automation Flow

| Step | Action |

|---|---|

| Step 1 | Salary credited |

| Step 2 | SIP auto-debited (within 3 days) |

| Step 3 | Bills + expenses managed |

Benefits

| Problem | Solved By Automation |

|---|---|

| Forgetting to invest | Auto SIP |

| Market timing | Eliminated |

| Emotional decisions | Reduced |

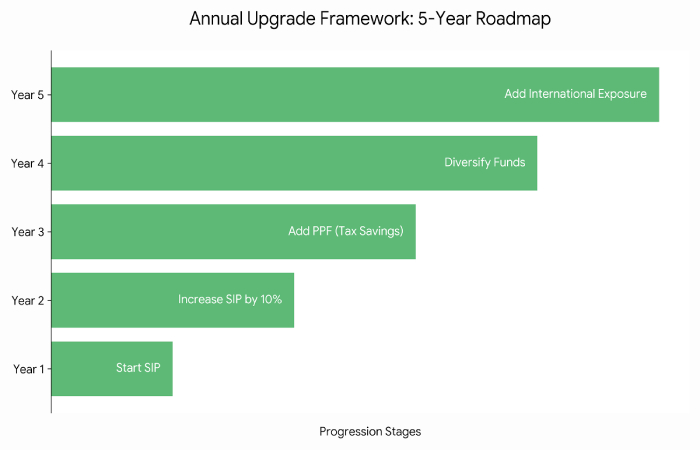

Step 8: Annual Upgrade Framework

Your investment plan should evolve yearly.

| Year | Action |

|---|---|

| Year 1 | Start SIP |

| Year 2 | Increase SIP by 10% |

| Year 3 | Add PPF |

| Year 4 | Diversify funds |

| Year 5 | Add international exposure |

Step 9: Risk & Market Reality

Markets are volatile. That’s normal.

Historical Market Falls

| Event | Market Drop | Recovery Time |

|---|---|---|

| 2008 Crisis | -50% | ~5 years |

| COVID Crash | -35% | <1 year |

Investor Behavior Impact

| Action | Outcome |

|---|---|

| Panic selling | Loss |

| Staying invested | Recovery + gains |

Step 10: 5 Year Execution Plan

If you’re serious about solving “i’m 25 and earning ₹30k a month how should i start investing for long-term growth?”, follow this roadmap:

| Phase | Focus | Investment Level |

|---|---|---|

| Year 1–2 | Build emergency fund | ₹3K–₹5K SIP |

| Year 3–4 | Increase investments | ₹6K–₹10K SIP |

| Year 5 | Diversify | ₹10K+ SIP |

Common Mistakes to Avoid

| Mistake | Why It’s Dangerous | Better Alternative |

|---|---|---|

| Waiting for right time | Misses compounding | Start now |

| Over-diversifying | Reduces returns | Keep 2–3 funds |

| Trading frequently | High risk | Long-term investing |

| Ignoring inflation | Wealth erosion | Equity exposure |

What Actually Builds Wealth

“i’m 25 and earning ₹30k a month how should i start investing for long-term growth?”

The answer is not in finding the “best” investment.

It’s in building a repeatable system:

| Component | Role |

|---|---|

| Consistency | Drives compounding |

| Time | Multiplies returns |

| Income growth | Accelerates wealth |

| Discipline | Prevents mistakes |

Conclusion

While starting with 30k/month at 25 isn’t the end of the world, it could actually benefit you if done at the right time and in a disciplined manner. A basic system to follow: discipline expenses, build an emergency fund, and consistently invest through SIPs in index funds with a low expense ratio, along with something stable such as PPF.

Never look for short-term returns of high percent and fashionable funds but increase the income you gain from and year on year increase in investment amount step-by-step. There will be no market timing, or picking individual stocks, what really counts over a period of time will be steadily investment and patience.